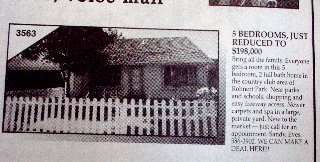

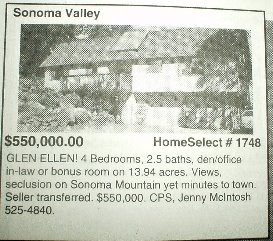

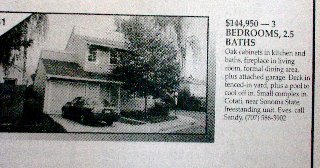

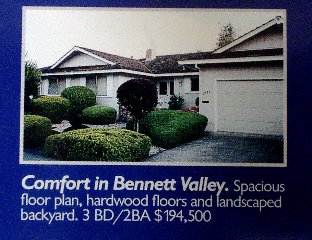

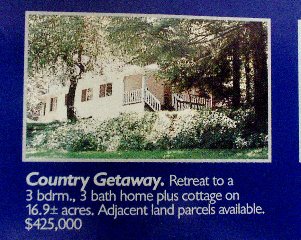

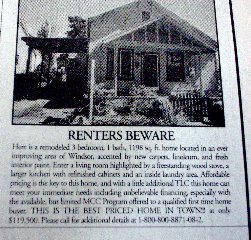

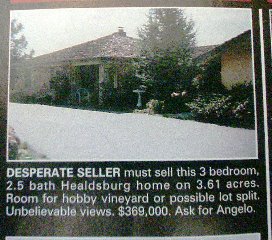

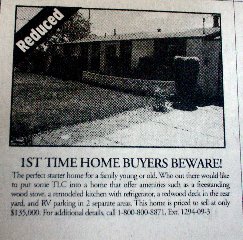

Headlines From the Last Crash

err... Was it a "soft landing?" Ah... who're we kidding... it was a crash. Though in comparison, it will probably will be looked at as one much smaller than this one will be.

Thank you MoonValley!!!

posted by Athena @ 3:56 PM

![]()

![]()

10 Comments:

Those headlines seems to betray what today would be considered uncharacteristic honesty. The good 'ol days.

I love those ads that I saved. They're from a time when buying was many times a better deal than renting, because there wasn't much difference between the two.

right... even in the non-crash years the delta was minimal... it was a time when home buyers really was something you worked to afford... and buyers had really been able to afford the houses... well, until they lost their jobs at least. But still... there was a time when having a job and making a six figure salary meant that you could afford to buy a house.

Now one can qualify for a jumbo loan... but it does not mean you can afford it.

great finds MV!!! Glad you saved these!

i heard a few minutes of a real estae show on ksro today...prices are "flat" and "may stay that way for a little while" the broker claimed 8-10% declines in the last downturn....this is so much bigger,and riskier,and so much of our economy is based on home appreciation and construction that i fail to see how anyone could call it anything but a disaster.not very many people will be positioned to take advantage of the situation for some years.i expect an overcorrection,as is usual, and 2001 prices in 3 years would be no surprise to me.

Tom... can you get the cash out refi data for Sonoma County?

I heard from the that the areas with the greatest price appreciations did not get their gains from actual prices and value increasing but due instead to the cash out refi's that made them drive up the price of their home.

So the official word is that this IS indeed a pyramid scheme. Put it all on the house and hand it off to the next fool in line.

i would have to get that data from a title company...perhaps some anonymous person could pull it.the people i know would be reluctant to jeopardize their jobs.as to how much influence cash out refies have had...i question it,the appraiser is still looking at "market value" one or two crooked appraisers per county would have a greater effect...cascading greed and nonexistent lending standards combined with "hey i don't want to hear it" are enough.appraisers are stuck...appraisals are based on comps...and most sfh appraisals consist of a few recent comps and a couple of photos of the exterior,because that is a)what the lender wants,and will pay for. and b)what the uniform standards of professional appraisal practice call for.it is always an opinion of a defined value as of a specific date.so you get an uniform residential appraisal report,with pictures,ta-da.julie speakes usually also includes a gross monthly rental multiplier,with a comment as to whether it is consistent with other recent sales in the neighborhood...a very polite way of noting that the market price is insane...few notice,fewer care.

Tom... can you get the cash out refi data for Sonoma County?

Could you get it for Marin County as well? That is, if you have an inside track which I don't.

no i can't get the data,i asked one person i trust she said no,already worried about layoffs...maybe take a bouquet of roses in to the title company...try a little flattery?are you good at that kind of stuff marinite?...i'm soso.i have one more person i can ask discreetly,but she is out of town...finally got out of a house in the valley she bought 5 years ago...sge's been sweating blood since december...fell out of escrow twice got 60k less than the first buyer offered...and very happy to take it.

marinite,i have been thinking about cash-out refi data,this would have to include heloc's,and here is the problem with that,the assessor's office and title companies would show the total amount of the line of credit,not the amount used. the "utilization rate" is a key factor in judging risk,and a risk analysis is of course the purpose getting this data.a title company could provide a zip code sorted list of cash out refi's from 2003 to the present,but then to get useful data,you would have to go to the credit bureaus to get zip sorted data of the # of helocs,average balance and utilization rates to have meaningful information.this struck me because a number of people i know have lines of credit for emergencies,which have been unused for years...but the title co still shows it as a $150k 2nd.i think that if you got the # of helocs for a zip,the percentage unused,and a range of use figure...what percent of people are under 25% utiliztion,50%,75% and maxed out...you would have something to work with.always nice to have adequate,appropriate data,of acceptable reliability...unless you are a reporter for the pd.

Post a Comment

Subscribe to Post Comments [Atom]

<< Home