Classic Market Failure

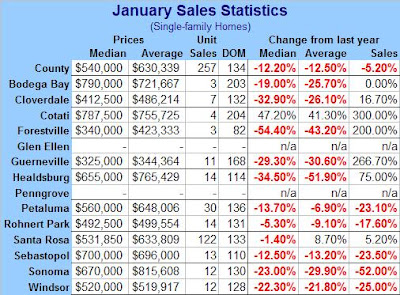

"Sonoma County's sagging housing market showed no signs of stabilizing in January as sales remained at a 10-year low and the median price fell 12 percent."

"Resale prices for single-family homes have fallen seven consecutive months when compared with a year earlier, the longest decline since 1993."

"In the Bay Area, sales of all new and resale homes and condominiums fell 4.1 percent in January, according to a report issued Thursday by DataQuick Information Systems. Sonoma County registered the deepest decline among the region's nine counties."

Remember, DataQuick reports foreclosure trustee sales as sales, so their data is highly suspect and the real number of sales is significantly lower than they are reporting. Therefore the % of sales falling is larger. Also, that impacts the sale prices they report as well since the loan amount is reported as a sale for the properties in foreclosure. Rigged system.

According to www.realtytrac.com

Sonoma County has: 938 properties in various stages of foreclosure

210 properties in Pre-Foreclosure

102 up for Auction

296 Bank Owned

297 are listed as resale

30 are new homes

3 are for sale by owner

www.foreclosure.com reports: 550 in foreclosure & preforeclosure

"Already one of the region's least affordable places to live, Sonoma County has fared worse largely because the local economy is the Bay Area's weakest."

"The county, which has one of the region's largest gaps between incomes and home prices, suffered job losses and poor income growth in summer and fall, further dampening demand for home purchases."

In 2006 only 7% of Sonoma County residents could afford a median priced home.

"Spring looms as a key indicator of where the market is headed, said Timothy Hedges, broker-manager for Prudential California Realty in Sebastopol."

"I don't feel the bottom of the market has occurred. I think it's going to be a little while," said Nick Dunlop, an appraiser who has pegged home prices in the county for 15 years. "It really was an eye-opener for me," he said.

"Many appraisers are lowering prices about 1 percent each month, Dunlop said."

"Price declines have not been enough to revive sales, largely because many families still cannot afford to purchase the typical home here. There also has been a psychological stalemate of sorts between sellers, who were slow to cut prices, and buyers, who remain cautious about paying too much."

www.ziprealty.com reports: 876 Sonoma County properties on the price reduced list.

'"The buyers that are out there are aggressively looking at really the comparable sales. They want to know what things have actually sold for. Base it on realistic sales, not maybes or what the neighbors are asking," Cary Fargo, a California Prudential Realty agent said."

"In another tactic, sellers are increasingly pulling their homes off the market for at least a month and putting them back up for sale as a new listing, perhaps at a lower price. The aim is to remove the stigma that the home couldn't sell, but agents can find a listing's full history."

"This trend was revealed by recent fluctuations in the supply of homes for sale in the county. The supply had been sticking in the six-month range, dropped to about four months in December, and then bounced back up to six months in January. Despite such maneuvers, the average number of days a home stays on the market before selling continues to rise."

The time it takes from when a home is listed for sale and put under contract: 134 days. a new record high.

"The supply of homes for sale should increase with the approach of the typically busier spring sales season."

Norcalmls: 2974 listings in Sonoma County

"U.S. Census Bureau data show that in 1979 the Bay Area median home price of $99,600 was almost five times the median household income. In 2005, the median home price of $645,300 was almost 10 times the median income. Not only does this wider gap make it more challenging to buy a home, it has altered the social dynamics of towns. "

Cynthia Kroll, senior regional economist at the Fisher Center for Real Estate and Urban Economics at UC Berkeley, who has been studying the California economy and real estate market for more than 20 years.

"With such a wide gap between home prices and incomes, there's a natural migration away from economic centers like San Francisco as people search for more affordable housing. The trade-off is usually a longer commute."

No Relief At North Bay Commuter Bottleneck

The California Transportation Commission recommended spending $141 million for car pool lanes on U.S. Highway 101 between Rohnert Park and Windsor River Road in Sonoma County.The recommendation is to widen the freeway from four to six lanes in both directions between Railroad Avenue and Windsor River Road. The Metropolitan Transportation Commission nominated the projects for funding.

However, the commission recommended not including the Marin-Sonoma Narrows widening project that would add two lanes in each direction to U.S. Highway 101 between Atherton Avenue in Novato and state Highway 116 in Petaluma.

The California Transportation Commission also didn't include a 4.1-mile, $30 million widening project along U.S. Highway 101 between state Highway 37 and Delong Avenue north of Atherton Avenue in Novato.

Bay Area home sales fell in January for the 24th straight month, and prices dropped to their lowest level in a year and a half.

"Last month's sales were the lowest for any January in 11 years, according to DataQuick. Compared with December, sales in January were down 26.3 percent."

"The Bay Area's falling housing prices match what is happening across the country. According to the National Association of Realtors, sales declined by 10.1 percent nationwide in the fourth quarter compared with the same period a year ago."

California was among the states with the biggest sales declines from October through December. National Association of Realtors reported, 40 states had drops in sales.

Sonoma County saw its median price fall 10.4 percent .

"Could lax underwriting standards during the housing boom years -- no verification of applicants' incomes or assets, low or no down payments, and big mortgages to people already saddled with heavy debt -- finally be coming home to roost?"

The omens are unmistakable:

"Delinquencies in the $1.3 trillion impaired-credit mortgage market hit 12.6 percent in the latest quarter, up from 11.7 percent. Delinquencies exceeded 13 percent among borrowers with subprime adjustable-rate loans."

"Growing numbers of the companies that make or invest in subprime mortgages are themselves facing financial distress, and some have shut their doors or filed for bankruptcy protection."

"HSBC Holdings PLC, Europe's largest bank and a major subprime lender in this country, shocked Wall Street recently by announcing that home loan delinquencies have gotten so bad that it has set aside $10.6 billion to cover potential losses."

"New Century Financial Corp., a subprime lender in California, saw its stock plunge 36 percent in a single day when it said "buybacks" of delinquent loans have been more numerous -- and more costly -- than anticipated."

"Ownit Mortgage Solutions, another high-profile California subprime mortgage lender, abruptly went out of business when buyback demands reached a reported $100 million."

"Dozens of smaller subprime originators have ceased operations or are scaling back on new lending. One of the mortgage industry's top executives, Angelo Mozilo, CEO of Countrywide Financial, was quoted as saying "there's probably 40 or 50 (subprime loan originators) a day throughout the country going down in one form or another. And I expect that to continue throughout the year."'

'"At a recent Senate hearing, a leading consumer-protection advocate, Martin Eakes, CEO of the Center for Responsible Lending, called the subprime market "a quiet but devastating disaster." '

"The "ultimate effects are very much like Hurricane Katrina," he said, but "the difference is that this disaster ... is occurring every single day across the country, house by house and neighborhood by neighborhood."'

“In recent months, as home-price appreciation fell and borrowers faced rising interest rates, more people defaulted on their mortgages. Under mortgage contracts, mortgage originators must often repurchase loans that default very early in their term or that come with underwriting mistakes, such as flawed property appraisals.”

“‘Following early payment defaults, we exercised our contractual rights to return loans to ResMae and protect our financial interests,’ a Merrill spokesman said.”

"Accredited Home Lenders has had to come up with more cash after getting margin calls from some of its warehouse lenders, Stuart Marvin, executive vice president at the subprime specialist told analysts during a conference call on Wednesday.”'

“‘We have eight different warehouse lenders; I would say the majority of them are acting very rationally,’ Marvin said. ‘There is one that is acting somewhat irrationally, although I won’t mention them by name.”

Industry publication "National Mortgage News said this week that Merrill Lynch has been making margins calls. A Merrill spokesman declined to comment. In late January, J.P. Morgan CEO Jamie Dimon noted rising defaults in some of its riskiest home loans and said the bank had largely exited the subprime business.”

“In another sign of growing concern about mortgages made to high-risk borrowers, Standard & Poor’s said it would no longer wait for homes to be foreclosed on and sold at a loss before alerting investors in mortgage-backed bonds that it expects to lower ratings on the bonds.”

“‘In terms of performance, I’d say there are equal concerns’ about Alt-A loans and sub-prime loans at S&P based on early delinquencies, said Ernestine Warner, an S&P analyst. The Alt-A bond S&P warned about was issued by Calabasas-based Countrywide Financial Corp., the largest U.S. mortgage lender. Newport Beach-based Impac Mortgage Holdings Inc. made the loans.”

“Mortgages were written for a fee, sold to investment banks for a fee, then packaged and floated for another fee. At each link in the chain, the fees mattered more than the quality of the loans, which could always be passed on.”

“‘This was classic market failure,’ says Anthony Sanders, a mortgage expert at Ohio State University’s Fisher College of Business. ‘The private sector wanted fees and got them, and they did not much care what happened afterwards.’”

“Countrywide and Washington Mutual face some risks from so-called ‘recastings’ of pay-option ARMs. Unlike fixed-rate loans, which have decades of underwriting data behind them, pay-option ARMs haven’t been stress-tested in an environment where home-price appreciation is slowing, and even falling in some regions of the country.”

“Roughly 28% of Washington Mutual’s loans held are in these riskier option-ARM mortgage products, according to S&P analyst Stuart Plesser. By contrast, pay-option loans comprise more than 40% of Countrywide’s interest-earning assets.”

posted by Athena @ 11:46 AM

![]()

![]()

15 Comments:

gee mr plesser,i hope you didn't hurt anyone's feelings at world savings or downey savings and loans by not mentioning them.my goodness,fee driven?who'd a thunk it...and what is this about selling folks on high risk loans? shoot they just gave folks what they wanted it's no different than the crack dealer at the playground...no demand ,no sales.

God i wish we could have big fat red negatives like that here in Marin. When?

Sorry Marinite. :-( As much as we don't want to think about it, Marin has been stretching itself less than the surrounding geographical areas. At least they have a pattern of actually being able to afford their houses enough to hold on to them. People who moved to marin for many years did so on purpose. The average income is higher, and the average household income is higher. So I think they will hold on just a little bit longer. Remember, this is just the first wave taking out the loose pebbles on the beach. These are the ones who had probably had NO business getting a credit card let alone a jumbo sized mortgage.

The next wave will take out those who are barely scraping by. Eventually the credit crunch will hit those that were doing well juggling money. Some really have been living off the house ATMs and they can do that all the way until the appreciation dries up and credit becomes near impossible to get for people who are too heavily leveraged.

I expect that the ones in trouble in marin would be those who jumped into the marin market in the last couple years. The next ones are the ones who've been spending their equity and using it to make ends meet believing when the Piper called they could refinance or sell because marin is a sure thing. (in their mind) I expect it to take a bit longer to have critical mass for this group.

When the credit cruch really sets in and people have to prove they can afford to repay the loan are the only ones who can get credit... Then you will have critical mass in Marin, because the buyer pool will dry up.

I know that of course. And Marin's market is so small the statistics are almost meaningless. I'm just sick of waiting and even more sick of blogging. Yoiu know I actually got a death threat by email the other day. I think it is time I cool it for a while.

I understand... did you see our sales? Good grief 12 in Sonoma, 12 in Windsor, 4 in Cotati. Only Santa Rosa and Petaluma had an impressive 30 and 122 sales. Yet the stupid press democrat's cheerleading real estate tools don't bother pointing out any of the real facts going on. Irritates me. :-/

good grief, people are threatening you? That is horrendous! 1. Report it. 2. Don't let the lame losers chase you off. You are a great reporter of reality and if someone hates the truth that bad, their bad choices will catch up with them.

I won't report it because if I do I lose my anonymity. Any one else with similar aims could then "finish the job". Besides, it was just a simple "if i ever find out who you are I will kill you" sort of thing. They are just trying to scare me off and, well, it worked.

...it was just a simple "if i ever find out who you are I will kill you" sort of thing."

Still, I have to wonder if they were "smart" enough to send that from their home IP or realty office. It's traceable, but would the police or FBI really bother?

You should be able to report to your ISP and have them go after the person. Don't let losers scare you off. Seriously. This is a lame action by a complete idiot. Who in the world reacts that way? That person has far more problems to be dealing with I am sure. If a blog makes them react in such a cowardly way, imagine how they are reacting in their real life. Don't give in to cowards. Report their email to your ISP. Also to the email service that they sent it to.

Crazy loser or not, it's not worth it to me. Crazy losers can still hurt you. And if I were to report this then I would probably become publically identifiable and then all the other crazy losers who got the idea might decide to act on it. Ok, so maybe I am a coward. Besides, this blogging thing is killing me (pun intended) and this latest incident just pushes me over the edge.

I just posted a blog entry on this letting them know they win.

Well I sincerely hope you change your mind. Please report it to your ISP and post their IP address on your blog. ;-) Send it to me and I will post the coward's IP address and have it traced as well.

I mean, this really freaks me out. I never really thought this sort of thing could happen. I know my posts are often strongly worded and yes, I deliberately try to be confrontational because I think that way people get more engaged in the issues. Maybe I got too carried away. Anyway, at the least I have to give it a rest for a while.

send me the loser's IP headers from the email anyway.

and no, you do not get too carried away. Also, your posts aren't even confrontational. You have a very common sense approach and someone would have to be a complete idiot to react the way this dipshit has behaved. I understand you are freaked, and perhaps a little downtime will lessen the impact you are feeling right now. I seriously hope so, because there will be a disturbance in the force without you on the blog scene.

Seriously, you are very graceful, insightful and intelligent RE reporting blogger.

This person is the dregs of humanity and doesn't deserve a narcissistic feed of even believing they have had such an impact on you. Irritates me to think this person now will believe their stupidity is useful.

:-/

send me the loser's IP headers from the email anyway.

Maybe, if I can figure out how. I'm going to sit on this for a while.

find the options in your email to show full headers. Copy and paste the full headers and email them to me. I know what to look for from there.

Post a Comment

Subscribe to Post Comments [Atom]

<< Home