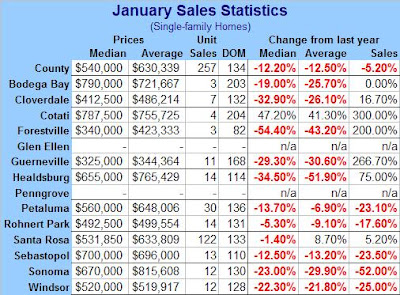

"Sonoma County's

sagging housing market showed no signs of stabilizing in January as sales remained at a 10-year low and the median price fell 12 percent."

"Resale prices for single-family homes have fallen seven consecutive months when compared with a year earlier, the longest decline since 1993."

"In the Bay Area, sales of all new and resale homes and condominiums fell 4.1 percent in January, according to a report issued Thursday by DataQuick Information Systems. Sonoma County registered the deepest decline among the region's nine counties."

Remember, DataQuick reports foreclosure trustee sales as sales, so their data is highly suspect and the real number of sales is significantly lower than they are reporting. Therefore the % of sales falling is larger. Also, that impacts the sale prices they report as well since the loan amount is reported as a sale for the properties in foreclosure. Rigged system. According to www.realtytrac.comSonoma County has: 938 properties in various stages of foreclosure 210 properties in Pre-Foreclosure102 up for Auction296 Bank Owned 297 are listed as resale30 are new homes3 are for sale by ownerwww.foreclosure.com reports: 550 in foreclosure & preforeclosure"Already one of the region's least affordable places to live, Sonoma County has fared worse largely because the local economy is the Bay Area's weakest."

"The county, which has one of the region's largest gaps between incomes and home prices, suffered job losses and poor income growth in summer and fall, further dampening demand for home purchases."

In 2006 only 7% of Sonoma County residents could afford a median priced home. "Spring looms as a key indicator of where the market is headed, said Timothy Hedges, broker-manager for Prudential California Realty in Sebastopol."

"I don't feel the bottom of the market has occurred. I think it's going to be a little while," said Nick Dunlop, an appraiser who has pegged home prices in the county for 15 years. "It really was an eye-opener for me," he said.

"Many appraisers are lowering prices about 1 percent each month, Dunlop said."

"Price declines have not been enough to revive sales, largely because many families still cannot afford to purchase the typical home here. There also has been a psychological stalemate of sorts between sellers, who were slow to cut prices, and buyers, who remain cautious about paying too much."

www.ziprealty.com reports: 876 Sonoma County properties on the price reduced list.'"The buyers that are out there are aggressively looking at really the comparable sales. They want to know what things have actually sold for. Base it on realistic sales, not maybes or what the neighbors are asking," Cary Fargo, a California Prudential Realty agent said."

"In another tactic, sellers are increasingly pulling their homes off the market for at least a month and putting them back up for sale as a new listing, perhaps at a lower price. The aim is to remove the stigma that the home couldn't sell, but agents can find a listing's full history."

"This trend was revealed by recent fluctuations in the supply of homes for sale in the county. The supply had been sticking in the six-month range, dropped to about four months in December, and then bounced back up to six months in January. Despite such maneuvers, the average number of days a home stays on the market before selling continues to rise."

The time it takes from when a home is listed for sale and put under contract: 134 days. a new record high."The supply of homes for sale should increase with the approach of the typically busier spring sales season."

Norcalmls: 2974 listings in Sonoma County

"U.S. Census Bureau data show that

in 1979 the Bay Area median home price of $99,600 was almost five times the median household income. In 2005, the median home price of $645,300 was almost 10 times the median income. Not only does this wider gap make it more challenging to buy a home, it has altered the social dynamics of towns. "

Cynthia Kroll, senior regional economist at the Fisher Center for Real Estate and Urban Economics at UC Berkeley, who has been studying the California economy and real estate market for more than 20 years.

"With such a wide gap between home prices and incomes, there's a natural migration away from economic centers like San Francisco as people search for more affordable housing. The trade-off is usually a longer commute."

No Relief At North Bay Commuter BottleneckThe California Transportation Commission recommended spending $141 million for car pool lanes on U.S. Highway 101 between Rohnert Park and Windsor River Road in Sonoma County.The recommendation is to widen the freeway from four to six lanes in both directions between Railroad Avenue and Windsor River Road. The Metropolitan Transportation Commission nominated the projects for funding.

However, the commission recommended not including the Marin-Sonoma Narrows widening project that would add two lanes in each direction to U.S. Highway 101 between Atherton Avenue in Novato and state Highway 116 in Petaluma.

The California Transportation Commission also didn't include a 4.1-mile, $30 million widening project along U.S. Highway 101 between state Highway 37 and Delong Avenue north of Atherton Avenue in Novato.

Bay Area home

sales fell in January for the 24th straight month, and prices dropped to their lowest level in a year and a half.

"Last month's sales were the lowest for any January in 11 years, according to DataQuick. Compared with December, sales in January were down 26.3 percent."

"The Bay Area's falling housing prices match what is happening across the country. According to the National Association of Realtors, sales declined by 10.1 percent nationwide in the fourth quarter compared with the same period a year ago."

California was among the states with the biggest sales declines from October through December. National Association of Realtors reported, 40 states had drops in sales.

Sonoma County saw its

median price fall 10.4 percent .

"Could

lax underwriting standards during the housing boom years -- no verification of applicants' incomes or assets, low or no down payments, and big mortgages to people already saddled with heavy debt -- finally be coming home to roost?"

The omens are unmistakable:

"Delinquencies in the $1.3 trillion impaired-credit mortgage market hit 12.6 percent in the latest quarter, up from 11.7 percent. Delinquencies exceeded 13 percent among borrowers with subprime adjustable-rate loans."

"Growing numbers of the companies that make or invest in subprime mortgages are themselves facing financial distress, and some have shut their doors or filed for bankruptcy protection."

"HSBC Holdings PLC, Europe's largest bank and a major subprime lender in this country, shocked Wall Street recently by announcing that home loan delinquencies have gotten so bad that it has set aside $10.6 billion to cover potential losses."

"New Century Financial Corp., a subprime lender in California, saw its stock plunge 36 percent in a single day when it said "buybacks" of delinquent loans have been more numerous -- and more costly -- than anticipated."

"Ownit Mortgage Solutions, another high-profile California subprime mortgage lender, abruptly went out of business when buyback demands reached a reported $100 million."

"Dozens of smaller subprime originators have ceased operations or are scaling back on new lending. One of the mortgage industry's top executives, Angelo Mozilo, CEO of Countrywide Financial, was quoted as saying "there's probably 40 or 50 (subprime loan originators) a day throughout the country going down in one form or another. And I expect that to continue throughout the year."'

'"At a recent Senate hearing, a leading consumer-protection advocate, Martin Eakes, CEO of the Center for Responsible Lending, called the subprime market "a quiet but devastating disaster." '

"The "ultimate effects are very much like Hurricane Katrina," he said, but "the difference is that this disaster ... is occurring every single day across the country, house by house and neighborhood by neighborhood."'

“In

recent months, as home-price appreciation fell and borrowers faced rising interest rates, more people defaulted on their mortgages. Under mortgage contracts, mortgage originators must often repurchase loans that default very early in their term or that come with underwriting mistakes, such as flawed property appraisals.”

“‘Following early payment defaults, we exercised our contractual rights to return loans to ResMae and protect our financial interests,’ a Merrill spokesman said.”

"Accredited Home Lenders has had to come up with more cash after getting margin calls from some of its warehouse lenders, Stuart Marvin, executive vice president at the subprime specialist told analysts during a conference call on Wednesday.”'

“‘We have eight different warehouse lenders; I would say the majority of them are acting very rationally,’ Marvin said. ‘There is one that is acting somewhat irrationally, although I won’t mention them by name.”

Industry publication "National Mortgage News said this week that Merrill Lynch has been making margins calls. A Merrill spokesman declined to comment. In late January, J.P. Morgan CEO Jamie Dimon noted rising defaults in some of its riskiest home loans and said the bank had largely exited the subprime business.”

“In another sign of

growing concern about mortgages made to high-risk borrowers, Standard & Poor’s said it would no longer wait for homes to be foreclosed on and sold at a loss before alerting investors in mortgage-backed bonds that it expects to lower ratings on the bonds.”

“‘In terms of performance, I’d say there are equal concerns’ about Alt-A loans and sub-prime loans at S&P based on early delinquencies, said Ernestine Warner, an S&P analyst. The Alt-A bond S&P warned about was issued by Calabasas-based Countrywide Financial Corp., the largest U.S. mortgage lender. Newport Beach-based Impac Mortgage Holdings Inc. made the loans.”

“

Mortgages were written for a fee, sold to investment banks for a fee, then packaged and floated for another fee. At each link in the chain, the fees mattered more than the quality of the loans, which could always be passed on.”

“‘This was classic market failure,’ says Anthony Sanders, a mortgage expert at Ohio State University’s Fisher College of Business. ‘The private sector wanted fees and got them, and they did not much care what happened afterwards.’”

“Countrywide and Washington Mutual

face some risks from so-called ‘recastings’ of pay-option ARMs. Unlike fixed-rate loans, which have decades of underwriting data behind them, pay-option ARMs haven’t been stress-tested in an environment where home-price appreciation is slowing, and even falling in some regions of the country.”

“Roughly 28% of Washington Mutual’s loans held are in these riskier option-ARM mortgage products, according to S&P analyst Stuart Plesser. By contrast, pay-option loans comprise more than 40% of Countrywide’s interest-earning assets.”